Gift Tax Planning Strategies in the U.S. (2025): Minimize Taxes & Maximize Wealth

Gift tax planning in the United States may seem complex, but with effective strategies, individuals may maximize their gifting potential while minimizing tax liabilities. This article explores the essential aspects of gift tax planning, including its definition, how it operates, methods to save on gift taxes, and strategic plans to preserve wealth while reducing tax exposure.

What is Gift Tax?

A tax document with “Gift Tax” highlighted, alongside financial paperwork

Gift tax is a federal levy imposed on the transfer of property or assets from one person to another without receiving something of equal value in return. The donor is responsible for paying this tax, but the Internal Revenue Service (IRS) offers exemptions that may allow individuals to transfer significant wealth without immediately incurring tax liabilities. These exemptions, including the annual exclusion and lifetime exemption, provide critical opportunities for effective tax planning.

How Does Gift Tax Work?

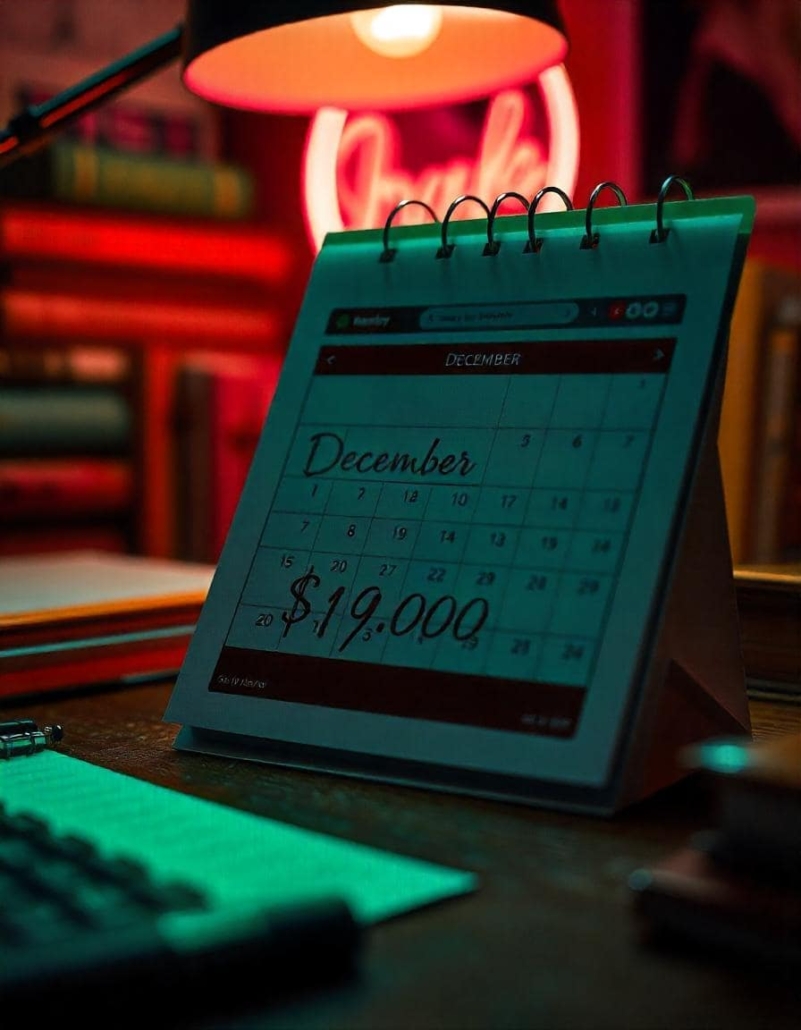

1. Annual Exclusion Limit

As of 2025, individuals can gift up to $19,000 per recipient, annually, without affecting their lifetime exemption. This means that taxpayers can distribute gifts to multiple recipients, each within this threshold of $19,000, without triggering gift tax.

2. Lifetime Exemption

Beyond the annual exclusion, the IRS allows a lifetime gift tax exemption of $13.99 million per individual for 2025. Gifts exceeding the annual exclusion count against this lifetime exemption. While this reduces the exemption available for estate tax purposes, it offers a significant shield against gift tax liabilities.

3. Taxable Gifts

If the cumulative value of gifts exceeds both the annual exclusion and the lifetime exemption, the donor may be subject to gift tax on the excess amount and is required to file IRS Form 709. However, with proper planning, exceeding these thresholds can often be avoided.

How to Save Taxes on Gifts

For individuals involved in cross-border mergers, gift tax planning becomes even more critical, as different tax jurisdictions may have varying regulations on wealth transfers.

1. Utilize Annual Exclusions Fully

Maximizing the annual exclusion is one of the simplest ways to reduce gift tax liability. By distributing gifts across multiple recipients, individuals can facilitate significant tax-free transfers. For example, a married couple may jointly gift up to $38,000 per recipient annually ($19,000 each), effectively doubling the tax-free transfer amount.

2. Fund Education or Medical Expenses

Payments made directly to educational institutions for tuition or medical providers for healthcare expenses, on behalf of another individual are not treated as taxable gifts. This method provides a unique opportunity to transfer wealth while limiting exposure to gift tax.

3. Gift Appreciated Assets

Transferring appreciated assets, such as stocks or real estate, is also a helpful tax-saving strategy. The recipient assumes the donor’s original cost basis, meaning potential capital gains tax is deferred until the asset is eventually sold. This approach may reduce the donor’s taxable estate while mitigating immediate capital gains tax consequences.

How to Plan Gift Tax on Property

While the USA does not impose a federal inheritance tax, some states have their own inheritance tax policies that individuals should consider when planning their gift and estate transfers.

1. Establish a Qualified Personal Residence Trust (QPRT)

A house inside a protective financial shield representing tax savings

A QPRT allows individuals to transfer ownership of their residence into a trust while retaining the right to live in the property for a specified term. Upon completion of term, ownership passes on to the beneficiaries. Since the IRS applies a discount based on the grantor’s retained interest, the taxable value of the gift may be reduced. If the grantor outlives the trust term, the property may be excluded from their taxable estate, leading to significant tax savings.

2. Consider Family Limited Partnerships (FLPs) or Limited Liability Companies (LLCs)

By transferring property into an FLP or LLC and subsequently gifting ownership interests to family members, donors can take advantage of valuation discounts for lack of marketability and minority ownership. This strategy may lead to a reduction in the appraised value of the gift for tax purposes, allowing more substantial transfers within the annual and lifetime exclusions. Proper structuring and compliance with IRS rules are essential for this approach to succeed.

Additional Tax-Saving Plans

Lifetime Gifting Strategy

Adopting a lifetime gifting strategy allows individuals to reduce their estate tax over time. By spreading out gifts over multiple years and recipients, donors can systematically transfer wealth while staying within annual exclusion limits.

Charitable Contributions

Donating property or assets to charitable organizations may qualify for a gift tax deduction. This approach not only eliminates gift tax liability but also reduces the taxable estate, benefiting both the donor and the chosen charity.

Conclusion

Gift tax planning is a vital part of effective wealth transfer and estate management. By leveraging tools like annual exclusions, lifetime exemptions, trusts, and valuation discounts, individuals can reduce their tax burdens while ensuring a smooth transfer of assets to their beneficiaries. Working with a tax advisor or estate planning professional is crucial to tailor these strategies to unique circumstances and ensure compliance with IRS regulations. Start planning today to make the most of gifting opportunities while preserving your legacy for future generations. For non-resident Indians (NRIs) with assets in the U.S., understanding tax for NRI is crucial, as different rules may apply to gift and estate taxes based on residency and citizenship status. Start optimizing your gift tax planning today! Consult with a tax expert to ensure a tax-efficient wealth transfer and secure your financial legacy.